Rosé, bubbles and English and British Wine are the bright sparks of an increasingly troubled UK on-trade sector, according to Peter McMcAtamney and his latest Wine Business Solutions’ Wine On-Premise UK 2023 report.

We keep hearing that restaurants in the UK are doing it tough. Cost of living pressure is impacting consumer spending. But you wouldn’t necessarily know that given what Brits are spending on wine in the on-trade. Here are some of the key findings from 2023 Wine Business Solutions’ Wine On-Premise UK report:

- The average price of a bottle of wine sold in the UK on-trade is now £44, up 9% and in line with inflation.

- The average price of a glass of white wine is up by 18% to £8.11 and red wine up 19% to £8.36. This indicates a strong opportunity for the UK on-trade to build back margins.

- Champagne listings are up by 45% on a year ago having dropped 10% year-on-year to the start of 2022.

- The rosé phenomenon shows no sign of slowing down with on-trade listings up 55% year-on-year with Provence driving the bulk of this growth.

- The one category that outshone all others is English and British wine. Listings are up by over 100% year-on-year which means for the first time WBS has enough data to make a statistically reliable assessment of British wine as a category.

- As a result British sparkling wine is now a bigger category than Cava in the UK on-trade something that would have been inconceivable a decade ago and highlights the difference between having a strategy that is driven by value over one that sells luxury. Aspiration always wins.

Country performance

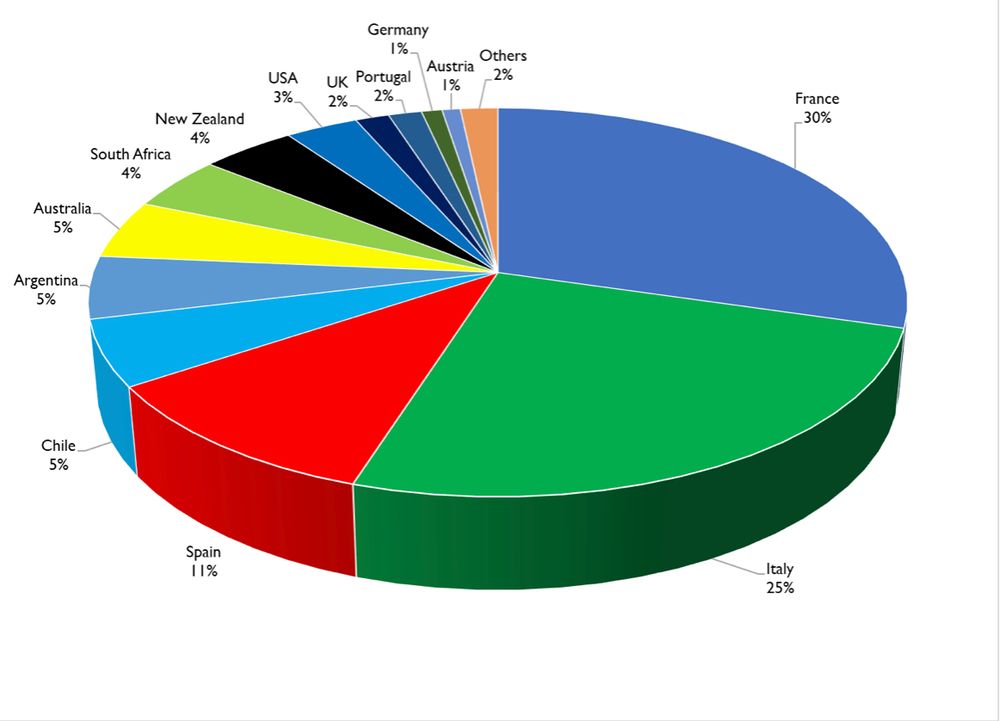

When we drill down into how the major wine producing countries are performing then it is the premium regions of France that are always in the best position to capitalise on any increase in wine spend, or trading up post lockdown.

Italy is still strengthening as it comes towards the end of a long run of increasing popularity. Spain, however, has just run through yet another fashion cycle, something it seems doomed to keep repeating. Whilst Portugal remains flat.

Looking further afield then Chile is losing significant ground, as it is in every market that WBS measures, as the market moves up and away from it, price wise.

Argentina, Australia and South Africa are all virtually unchanged from last year, whilst the US has enjoyed some growth. Each country is very different, however, in terms of internal category dynamics and likely future prospects.

Figure 1 – Share of Total Wine Listings by Country

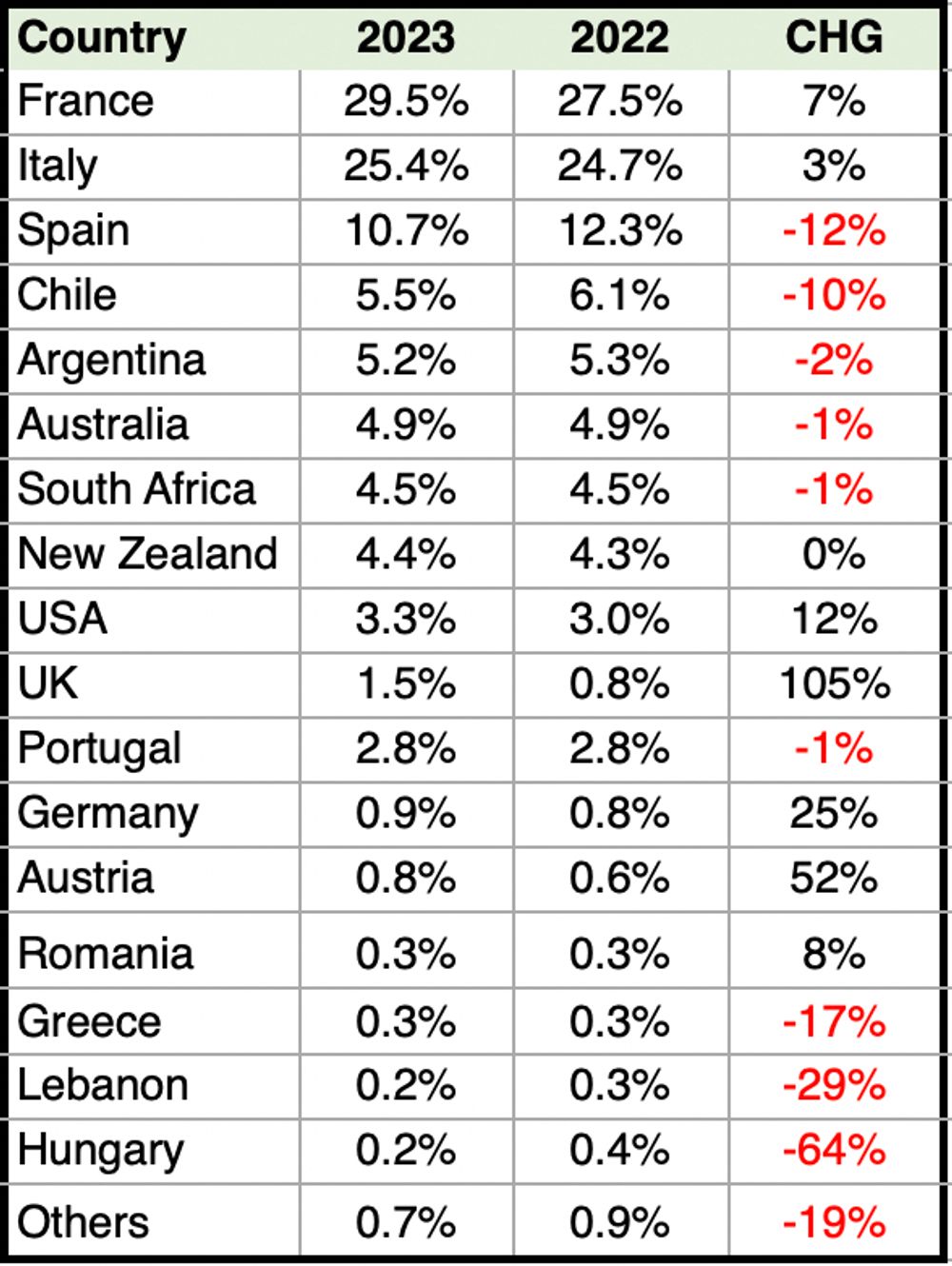

Figure 2 – Share of Total Wine Listings by Country – 2022 to 2023

As the market and prices have picked up, there is plenty of wine that is now starting to come into its own. This is particularly the case for Germany and Austria which reflects the average consumer being more open to discovery and trying new styles of wine post Covid. Austrian wine has done particularly well coming out of lockdown. This was true across all its major markets.Who would have thought that Romanian wine would become more popular than Greek wine?

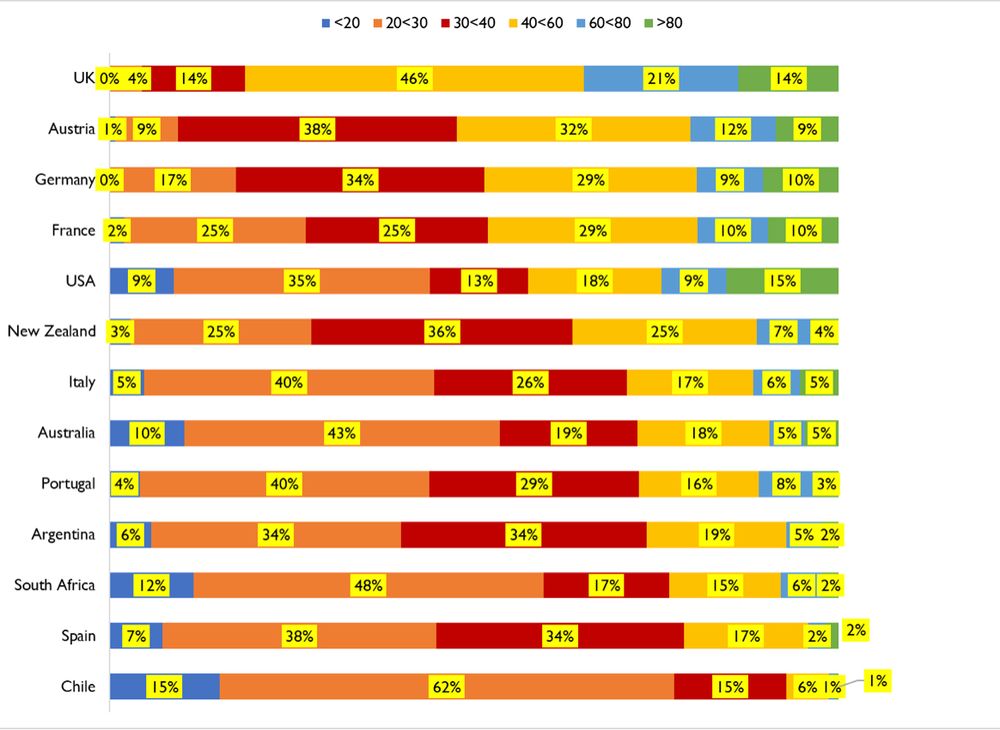

Figure 3 – Proportion of Listings at Price Points (£s per Bottle) by Country

Note – Excluding Champagne

If price correlates with image, then the UK wine industry is doing it better than anyone. Only 18% of its offer is listed at £40 per bottle or less. The average by-the-bottle price of UK wine now sits at £56.

Austria is the next best positioned country brand from a price and image perspective, its sales picking up nicely as the market heads back to premium. Germany prices its offer similarly.

France has the next highest proportion of wines listed at more than £40 per bottle and has the highest average price overall.

The challenge for Italy is to recalibrate its offer to better suit where the market is going.

The US wine offer has always been a bit of a ‘double barreled’ approach, strong at the bottom and top, but not much in the middle where profitable sales for medium sized wineries normally lie.

New Zealand has most of its wine pitched in the £20-40 space. New Zealand, however, has a lot more wines priced at over £30 and has increased prices, overall, significantly on the back of strong demand.

The figures also show Spain is suffering from not having a premium image, which is reflected in lack of premium wine sales at a time when the market is increasing prices.

South Africa, Australia and Argentina all sit well back for the market average. Chile, however, sets itself apart as the low-cost provider, the last place you want to be in market that is heading rapidly up in price.

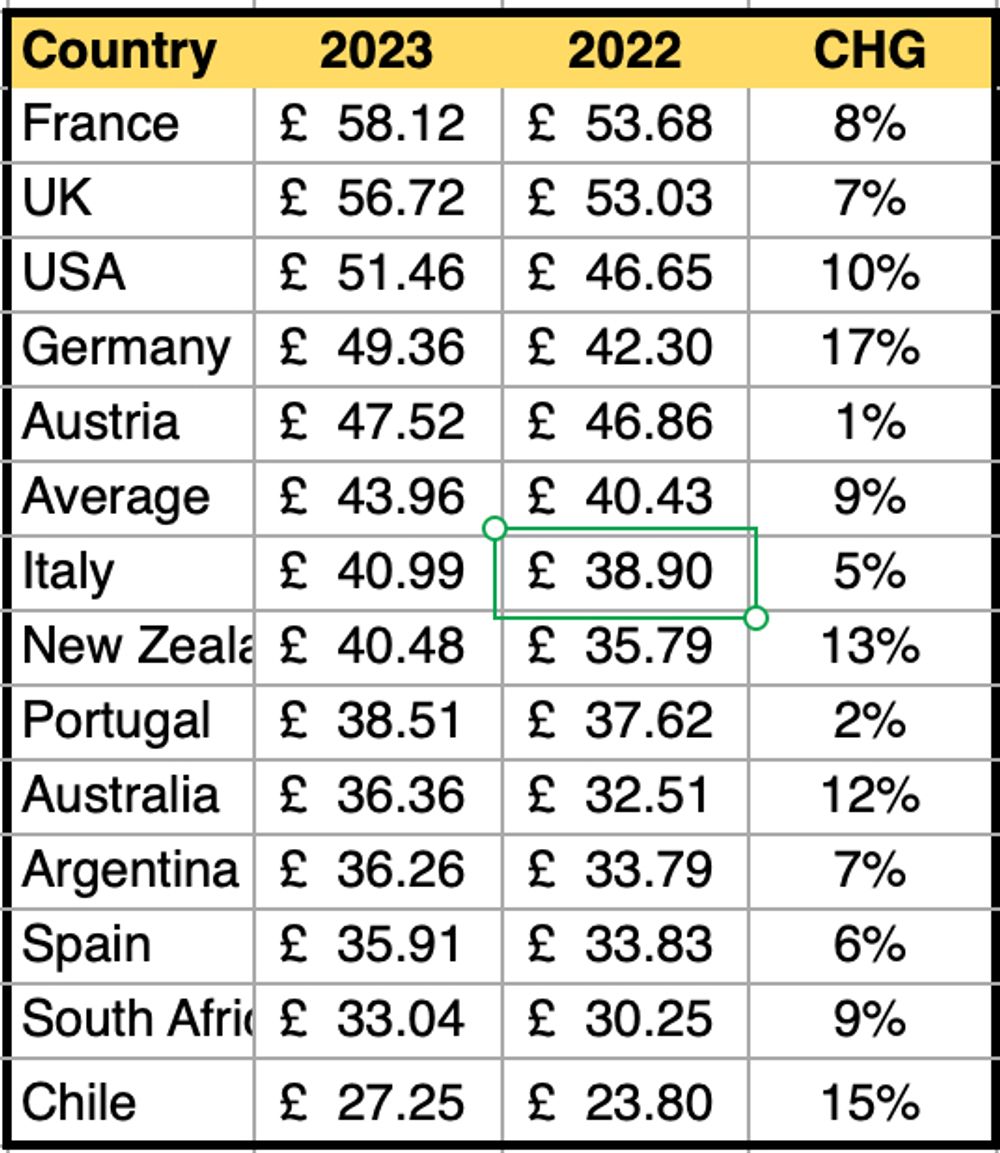

Figure 4 – The Average Listed Price of a Bottle of Wine by Country

Note – Excluding Champagne

Finally, our ‘Distributor of the Year’ was Berkmann Wine Agencies who outperformed all other major businesses in terms of both growth in share of listings and listings per brand carried.

- Wine Business Solutions On-Premise reports are designed to be the definitive guide as to who the best distributions are, what the most successful brands, countries and regions are and the price of wine across categories and regions on the UK. An extract of the report can be downloaded by following this link or to secure a copy simple follow this link. Contact peter@winebusinesssolutions.com.au if you have any questions.