In the first of a two part report analysing the state of the UK on-trade we talk to industry experts, leading on-trade suppliers and operators about who are the likely winners and losers in what is clearly a difficult marketplace. Part two of this report will examine the drinks and the wines that suppliers and restaurants need to be concentrating on.

It’s been hard to find a good news restaurant story in the last couple of months. Everywhere you turn there is another announcement from a major high street chain of major closures, cutbacks, and businesses going into administration. It’s clear the mid market, casual dining sector, so long the darling of the on-trade, is the one facing the most difficulty as chains that arguably expanded too quickly are now being hit by what is being seen as a perfect storm of rising costs, business rates, staff wages, and a drop in consumer spending.

The fact the casual dining closures are across the board in terms of style of cuisine and type of outlet, with the likes of Jamie’s Italian, Strada, Prezzo and Bryon all being hit, shows this is an industry issue rather than a change in what consumers are choosing to eat. The government’s own Insolvency Service reported 984 restaurants went to the wall in 2017 and we are still losing 18 to 20 pubs a week (CAMRA).

Jamie’s Italian was one of the highest profile casual dining chains to announce outlet closures this year

Consumer power

The core of the issue is consumer confidence. However you may have personally voted the looming prospect of Brexit, and what it means for the economy and people’s jobs is having a major impact on how and where we are spending our money. There are no so many more reasons not to go out in the evening, but stay at home with a bottle of wine or a few beers and a takeaway, and settle into the latest box set you are downloading on Netflix.

But it’s not only the potential cost that is stopping consumers from spending more on drinking. Increasing awareness and concerns over health are resulting in more people becoming teetotal or cutting down on their weekly units. Around a fifth of the UK population now don’t drink alcohol at all, with their abstemious ranks swelling by around 0.2% a year.

Liberty Wines reveals in its latest on-trade report released last week that its own consumer shows nearly half (47%) of people are more concerned about what impact alcohol is having on their health and that 45% are looking to cut back, both for health and religious reasons.

There is also a general trend towards moderation in both frequency and quantity of not just alcohol, but also the kind of unhealthy food the casual dining sector is renown for.

At the same time, competition is growing from food-only kitchen and delivery services such as Deliveroo that are changing the way we choose to eat restaurant food.

So rather than actually go in person to our favourite burger, pizza or Mexican restaurant we can get their food delivered right to our door. Which might be still good news for those type of restaurants, it is having a massive hit on the drinks sector as people are not ordering a bottle of wine, a cocktail or a beer to go with their order. Which, in turn, hits the restaurant’s bottom line as they do not have the drinks margins to help compensate for increased food and ingredient costs.

Rise of the meal kit

The rise of the meal kits at home like Hello Fresh are hitting in the eating out market

The likes of Deliveroo are also drawing investment capital away from more conventional restaurant concepts, points out Wine Intelligence in its UK On trade 2018 trends report. Rather than invest in another casual dining chain, the private equity investors are looking for the new kids on the block, the middle men, that can get restaurant food to people’s doors. Businesses that, stresses Wine Intelligence, are more low risk and less of a capital outlay than having to build a national network of restaurants.

Then there is the rise of the meal-at-home cook kits, like Hello Fresh, that are offering another alternative to eating out that is often a cheaper, fresher, healthier and ultimately more convenient way for consumers to expand their eating repertoire and cut costs at the same time.

What’s more many of these businesses are run on weekly subscription models that not only tap into the consumers’ growing desire to take more control of what they are spending and eating, but means it is a lot less likely that they are just going to pop out, mid-week, to the local Pizza Express, when they have fresh food ready to be eaten at home.

Impact on drinks

All these market dynamics that are working against the future of mainstream restaurants are equally bad news for the drinks industry that supplies them. You only need to look at the latest on-trade reports to see that.

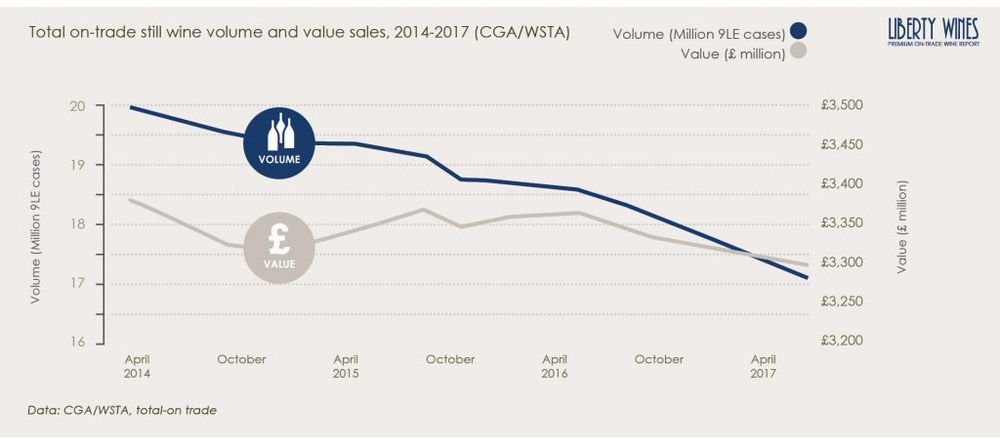

Accolade Wines, for example, reported earlier this month that overall UK on-trade wine volumes were down by 5% in 2017 on 2016, with value dipping by 0.5%. While all still wine categories fell, including a 7% drop in volume and 2% decline in red wine, it was only sparkling wine that was on the up, recording a massive 23.3% increase in volume and 22.7% increase in value.

The latest Liberty Wines on-trade report finds that the total premium UK on-trade wine market has contracted by over two million cases in the past three years and that in 2017 the total UK on-trade market saw volumes drop by 6% and value by 1%.

“Some restauranteurs also report that wine is receiving less attention as gin, cocktails and craft beer are attracting more consumers,” says Wine Intelligence’s chief operating officer, Richard Halstead. “Although wine remains the backbone of the alcohol on offer in most food-led outlets, these other drinks are more talked about and have grown in repertoire over the past year, while wine perception has remained the same.”

Premium on the up

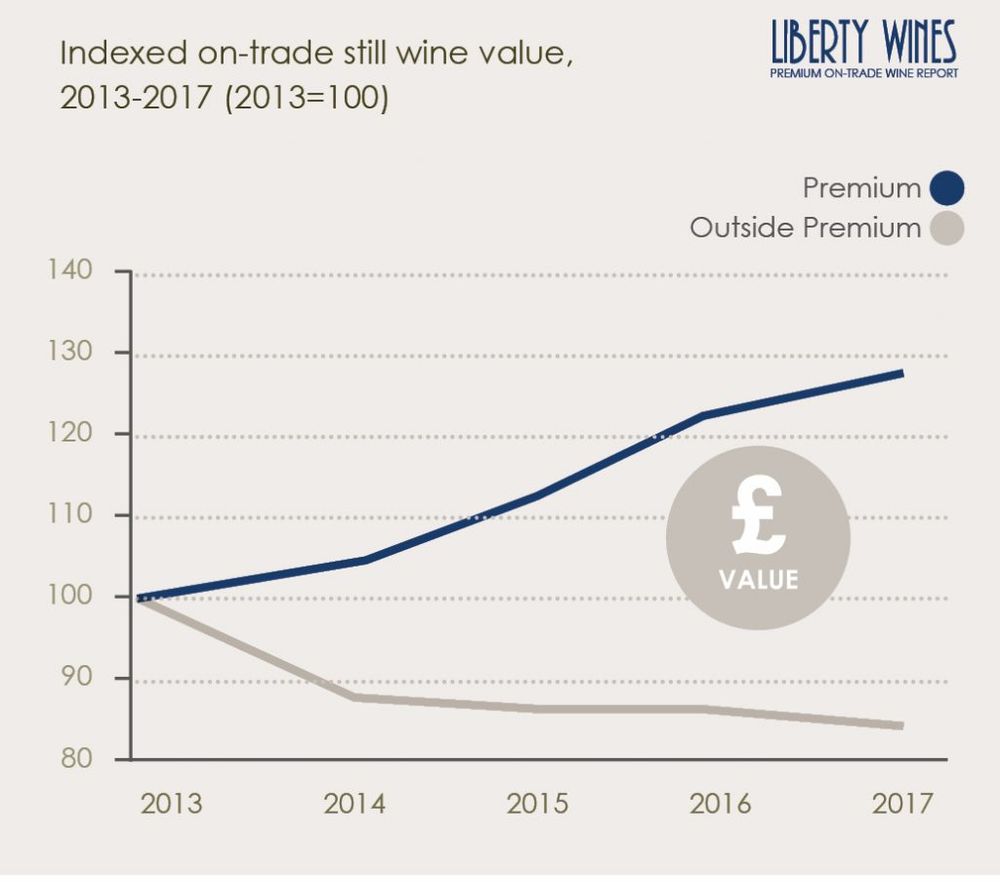

While overall wine sales may be down, the good news for the premium on-trade is that consumers are splashing out more on wine when they do go out, according to Liberty Wine’s annual report, produced in conjunction with CGA. It says the average bottle price has risen almost three times faster in the premium on-trade than in the rest of the on-trade since 2014.

“Our research shows value – quality at all price levels – is vitally important,” says Liberty Wines’ sales director Tom Platt. “This is illustrated by the continued rise of the average selling price.”

David Gleave MW, Liberty Wines’ managing director, adds that despite the prevailing uncertain economic climate, there still exist opportunities within the premium market for the on-trade to encourage consumers to be more adventurous and to drink better wine. Liberty’s research, for example, shows two thirds of consumers it surveyed would be willing to pay more for their favourite wine styles and would be more experimental if wine lists had clearer descriptions.

Richard Halstead concurs. “It’s hard to find a good news story in the UK on-trade at the moment, and wine is not immune from the cold winds sweeping through the sector,” he warns. “The message from our report seems to be that lazy or outdated wine offers are going to be punished, and rewards will accrue to those who are using the wine list as an opportunity to bring new knowledge and understanding to consumers.”

And despite all appearances to the contrary, opportunities in the on-trade do exist. For one thing, the premium sector of the on-trade is growing. Five years ago, it accounted for 7% by volume of the total on-trade market, and 10% of its value. Now, the premium on-trade comprises 10% of total volume and 14% of its value, says Liberty Wines.

What’s more that growth in premium sales is coming from all channels of the premium on-trade: restaurants; hotels; pubs; and wine bars. All of which continue to account for the majority of premium wine sales, adds Liberty Wines. Between them they have increased their market share of the premium on-trade from 57% to 70% since 2013, with restaurants accounting for 28% of the overall premium on-trade, hotels 24%, gastropubs, which have doubled to 10% to overtake wine bars, and the latter which now account for 9% of the sector.

The premium on-trade consumer

Its important for premium outlets to offer discerning and different wine lists to keep a predominantly younger audience engaged.

According to Liberty Wines, the most frequent visitors to the premium on-trade are 18-34 year olds. While nearly a third (29%) of premium on-trade wine drinkers say they want to try something new or different, over half (53%) don’t think that wine lists are generally well designed, nor are they helpful in finding the wines they want. And over 80% say that clear descriptions of how a wine tastes would makes it easier for them to choose something new or more expensive. So the message for the on-trade is loud and clear – get your wine list in order

“As indicated by our research, consumers want wine lists that present the information in a way that makes it as easy as possible for them to choose a great wine,” says Gleave. “A good on-trade buyer will understand what works best for their customers, whether that is to arrange by style or country, whether to include descriptions, or whether to list ten wines or a hundred or to invest in staff training to give staff the information they need to advise customers on the best wine to choose. There really is no single approach to take.

“However a wine list is arranged, appropriate staff training will help make the most of it. Knowledgeable staff can make all the difference between someone opting for the house wine or experimenting with a wine higher up the list.”

Size matters

Another factor for the on-trade to consider is serving wine in different sizes. Nearly a third of women in the Liberty survey (32%) said they would spend more if there were different sized servings, such as 500ml carafes or a smaller 125ml glass on offer. Similarly a third of those aged between 45-54 said they would be prepared to spend more if more wines by the glass were available. Meanwhile, the same proportion of men said they were more likely to splash the cash if there were food and wine pairings on offer.

Not surprisingly, the over 55’s were most likely to favour classic wines, and tended to be more knowledgeable than other age groups, requiring less advice and guidance. While they know what they like, the over 55’s also claimed to drink the widest range of red wine styles and varieties of any age group.

The London market

London, and the City in particular, does so much to drive premium on-trade trends for the rest of the country

With a population of over ten million, around double that of the whole of Scotland, London dominates the premium on-trade, accounting for over half (55%) of the sector’s total value. However, volumes have been sliding in the past year, particularly in white wines, though value has continued to grow, which is in line with the “less but better” trend seen elsewhere.

London drinkers are twice as likely to drink wine in the premium on-trade more than once a week, making them a good “barometer” of the category, according to Liberty Wines.

Average bottle prices have grown more quickly, and are 13% higher than in the rest of the country, with average prices of wines from Italy, New Zealand, Spain, the US and Australia disproportionately higher, and in some cases much more than the average 13% price premium. In addition, sales of sparkling wines are stronger in London, and consumers are more adventurous than outside the capital.

With white wine accounting for over half (56%) of the London market, Sauvignon Blanc has seen its market share grow over the past five years and continues to be the capital’s top selling variety. However, in the past year, volumes declined by 10% and value sales were flat.

Meanwhile, adventurous Londoners keen to try out new wines has resulted in increased demand for alternative varieties such as Sangiovese and Grenache. These alternatives accounted for only 18% of volume sales in 2013, but this leaped to 36% by 2017. This has been at the expense of more traditional varieties such as Merlot, which has seen volumes decline from a 33% market share five years ago to only 21% today.

London-based consumers are also increasingly embracing South African wines, which in the capital’s premium on-trade account for 8% of the market. Sales have increased by 12% in value against flat volumes, indicating that consumers are spending more on favourite varieties such as Chenin Blanc and Syrah.

And London wine drinkers are also increasingly switching onto non-fortified wines from Portugal, which have shown strong value growth with the average bottle price increasing as a result.

The regions

Liverpool, along with London, Bristol, Brighton, and Glasgow are all seen as key drivers in the premium on-trade outside London

As for the rest of the country, Liberty Wines reports that most of the premium on-trade has grown, though the market remains “more challenging” in the north.

The fastest growing area last year was the Midlands and Anglia, a region which accounts for around 16% of the premium on-trade still wine market, and which recorded a 30% increase in value of still wine last year, though sparkling wine was down by 10% in volume and 5% in value. Conversely, the north saw sales of still wine dip by 7% in volume and 4% in value, but sparkling wine sales climbed by a hefty 22% in volume and 25% in value.

In the South of the country, volumes of still wine were flat, though value nudged up by 7%, while sparkling wine sales dipped by 1% in volumes but plunged 17% in value, indicating that southerners are switching to cheaper fizz.

North of the border, sparkling wine is booming, with volumes and values both soaring by a dizzying 44% last year. However, this was not matched by the Scots’ enthusiasm for still wine, where volumes were down by 10% and value by 5%.

In the South West and Wales, still wine sales in the premium on-trade fell by 16% with value down by 12%, though sparkling wine saw volumes and value up by 5%.

- Part two of The Buyer’s analysis of the latest on-trade trends will concentrate on the countries, the styles, and the grape varieties that are winning in the premium on-trade.