Australia’s premium wine producers are on the front foot with new styles of wine, often made with alternative varieties and low intervention winemaking, which are slowly starting to eek some market share away from the still dominant high volume, commercial branded end of the market.

Australian producers are now looking to raise the stakes and put the focus on their premium wines

It’s always hard to get an accurate perception of what is happening in any particular country by spending a few hours at their annual generic tasting. By the very nature of these things the generic body, their producers and the importers they are working with are all trying to show you the best of what they have to offer. Which to a large degree was very much the case at last month’s this Wine Australia’s Trade Tasting in London.

It’s what Robert Joseph, the respected wine commentator, writer and wine producer, described as being the “tip of the iceberg” of what the country has to offer. But the good news for Australia is that the tip is growing and sticking out of the water far more so than it was say three to five years ago.

Yes, the majority of the wines available to taste were very much at the more mid to premium end of the Australian wine scene, but the fact there was so much to taste, across all regions, and where there seemed to be as many Sangioveses on display as there were Shirazes shows how far Australia has come and the direction where it is going in the future.

It certainly mirrored my own experiences of travelling across a number of the major Australian wine regions in November last year. Then, as with this week, the focus, was very much on what Australia is doing differently, with new alternative varieties and more traditional, minimum intervention winemaking techniques. There is now a lot to see, taste, discover and potentially buy if you are looking for wines pushing £10 and above.

There is no doubt Australia has turned the corner from what it would admit itself was the difficult, dark days of around five years ago when a combination of too much mass produced, commercial, formulaic wines and uncompetitive currency rates saw buyers move in their droves to other more interesting and commercially viable parts of the world. Whatever premium and fine wines it was producing were not being heard.

Even as prominent an Australian wine critic and commentator as Mike Bennie admitted to me during my recent trip that he had stopped even drinking Australian wine five years ago, or selling them at his Sydney wine merchants, P&V Wine & Liquor. Now his shelves are near breaking from them.

“About five years ago I was only drinking overseas wine. I had become bored with Australian wine. But the explosion in natural and unfiltered wine has revived my love in our wine and wines that are genuinely true to their place,” he explained.

Complete turnaround

Growth is coming from Australia’s premium price points

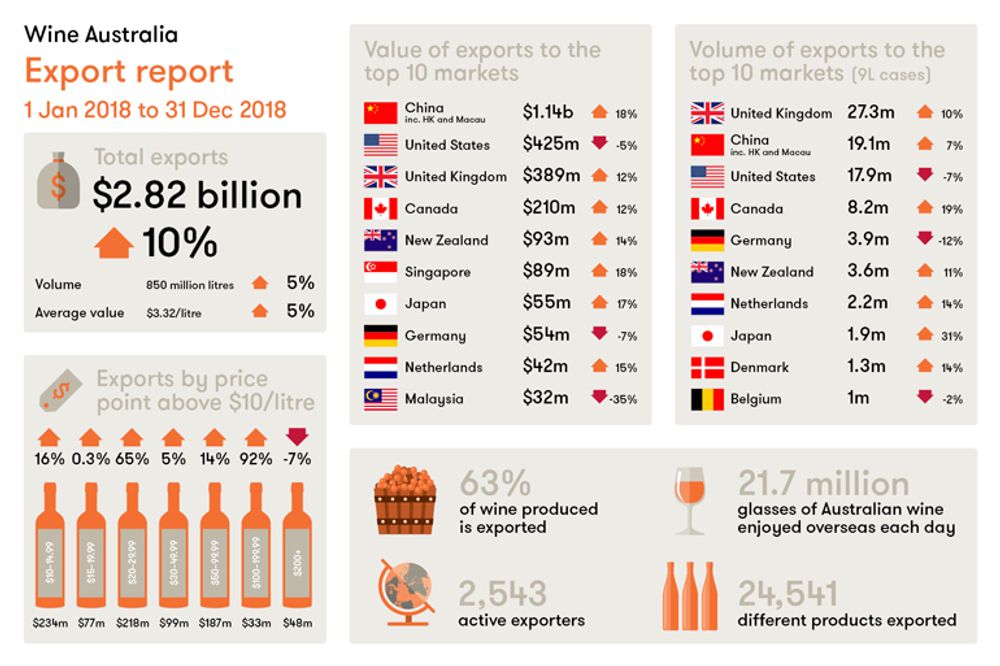

The picture now could not be more different. Global demand for Australian demand has been completely turned on its head since 2013. From a peak in 2007 of A$3bn worth of exports, it had slumped year, by year to around A$1.8bn in 2013, before being transformed back up to $2.82bn in 2018, a jump in the last year of 10%. Which equates to an average compound growth year-by-year of 10% for the last five years.

Of that A$2.82 billion it might surprise some to know that A$896m is for wines priced over A$10 with the fastest growing price sectors being A$10-A$14, up 16% to A$234m, A$20-A$29.99 up 65% to be worth A$218m and 14% jump for wines priced between A$50 and A$100, worth A$187m.

It’s not surprising Wine Australia’s chief executive, Andreas Clark, was in buoyant mood at this week’s tasting. “It’s a bloody exciting time,” he said and even went as far as calling it a “new epoch” for the Australian wine industry.

They might not be popping the Australian Prosecco just yet, but there is definitely more of a “quiet confidence” about what it is doing as a country, added Clark. “We are now proud of what we doing and have a great story to tell,” he said.

Clark admitted he probably won’t see it in his lifetime but the long term – 30 year – goal for Australia is to be “recognised as the world’s pre-eminent wine producing country”. Particularly as it currently only accounts for 4% of total wine production, compared to 17% for France and 15% for Italy.

Chinese demand

The free trade agreement signed between China and Australia has quietly changed the face of Australian exports

A lot of its turnaround has come thanks to the “phenomenal” rise of exports to China, helped be a free trade agreement that has been introduced on a sliding scale over the last few years, to reach zero in 2019, says Clark. It has resulted in 32% per annum growth into China for the last five years and although that fell back to 22% in 2018, that has to be seen in context of a natural re-positioning after so many years of growth, he stressed.

In 2012 Australia was shipping A$241m worth of wine to China. In 2018 that had jumped to A$1.14bn and leapfrogged above Canada, the UK and the US into by far its biggest international market. The US is now way back in second place with A$425m exports compared to A$450m in 2012. The UK has slipped back to third from A$401m in 2012 to A$389m in 2018.

Unusually for such a strong bulk, dominated industry it has been bottled rather than bulk that has led the way for Australia in China, making up 80% of its exports there. This is in direct contrast to how it has built its market share in the UK, which is still 80% dominated by bulk wine shipping.

The rest of the iceberg

But then there is the rest of the iceberg resting below the surface that we also have to consider as well. Where, after all, the vast majority of Australia’s wine production still sits. The on-going challenge is to get more of its wines above the water line and to places where they can drive long term sustainability right through the entire Australian wine supply chain.

It’s not all hunky dory, though. Far from it. The US remains the biggest factor on Australia’s ‘to do’ list. For all its efforts the US is not falling in love with Australia just yet. In 2018 volumes were down 7% to 17.9m 9 litre cases and value down 5% to A$425m. But there are signs, claims Clark, that there is at least a flirtation going on with sales up 1% in the last quarter in a year when overall value was down 5%. Its US off-trade performance is also encouraging with a 3.8% increase in the year to September 2018 in a sector that only grew 1.3%.

It will be vital for Australia’s long term ambitions for it to make bigger inroads into the US and it’s where Wine Australia is investing a large proportion of its marketing and promotional budget for the years ahead. The challenge, claimed Clark, was less with consumers, but getting through the three tier system and powerful distributors that help manage it.

Demand for food friendly wines across Australia, from Adelaide to Sydney is helping producers be more ambitious

In its other key markets the pendulum is still very much at the commercial end of the category. For all the talk and presence of more premium wines in the UK the stark fact is 90% of sales are still below £7. But there are more encouraging signs with one of the fastest growing UK price segments being between £6 to £7, where volumes were up 16% to break through 4m cases for the first time. Its challenge now is to push that up to between £7 to £8, where there was a 9% drop in volumes last year to under 1m cases. The biggest volume categories are £5 to £6, with over 7m cases, but down 0.4% and £4 to £5 at 5m cases.

What will be encouraging, though, for Australia is that its value performance in the UK was up 12% in 2018 to A$389m, which is by far the highest return in the last five years, and a big jump from 2017 when it slipped under A$350m.

That premium message is getting through even at the most commercial ends of the market, and with duty levels having gone up again at the end of last week, it simply is not economic for Australia to be batting too much below £4 or even £5, no matter how much it is asked to. Volume sales of Australian wine in the UK below £4 were down 46% in 2018.

Driving value

The encouraging aspect of Australia’s rise and return to form globally is that it is the value of its exports that is going up as well as its volumes. In 2012 its average price per litre of exported wine was A$2.57, in 2014 that had only crept up to A$2.60. Now in 2018 it is proudly sitting at A$3.32, up 5% on 2017.

If it can keep that average export price point pushing up then we will get to see more of Australia’s iceberg of wine above the water level, which can only be good news for the country as a whole.

Other key export figures

Markets with encouraging signs of growth

Netherlands, up by 15% to $42m

Denmark up by 19% to $25m

Sweden up by 13% to $42m

Australia’s top five exported varietals

Shiraz – A$662m, +11%

Cabernet Sauvignon – A$356m, +5%

Shiraz/Cabernet Sauvignon -A$231m, +22%

Chardonnay – A$184m, +5%

Cab Sauvignon/Shiraz – A$113m, +13%

Varietals on the rise in the UK (from a small base)

Imports of Australian Fiano are up 30% in value

Imports of Australian Vermentino are up by 29% in value

Imports of Australian Nebbiolo are up by 17% in value

Imports of Australian Pinot Noir are up by 8% in value

Varietals on the rise in Europe excluding UK

Imports of Australian Rieseling are up by 41% in value

Imports of Australian Pinot NOire are up by 31% in value

Imports of Pinot Grigio are up by 26% in value

Imports of Australian Grenache are up by 19% in value

Australian sparkling wine

Imports into UK are up by 2% by value

Imports into Europe are up by 12% in value

Australian rosé

Imports into UK are up by 17% in value

Imports into Europe are up by 66% in value

Source: Wine Australia

- This article has been adapted by one that was first published on VINEX, the bulk wine and private label trading site.